Is it better to save or pay off debt?

Whether it's from a tax refund, a gift from a family member, or a freelance project, extra cash isn't always easy to come by. So what you do with that income can make a big impact on your financial well-being.

Should you use it to build an emergency fund, save for a long-term goal like retirement, or pay off debt? Your answer depends as much on your financial objectives as it does your financial means. Here are four questions to help you determine whether it's best to save or pay off debt with your extra income.

1. How much do you have in savings?

If you have little savings, building an emergency fund might be your top priority. The general recommendation is to have three to six months of living expenses in an emergency fund to pay for unexpected costs like car or home repairs, medical bills, and emergency travel. This fund can also help support you in the event of unemployment, illness, or divorce, all of which can deliver a major financial blow.

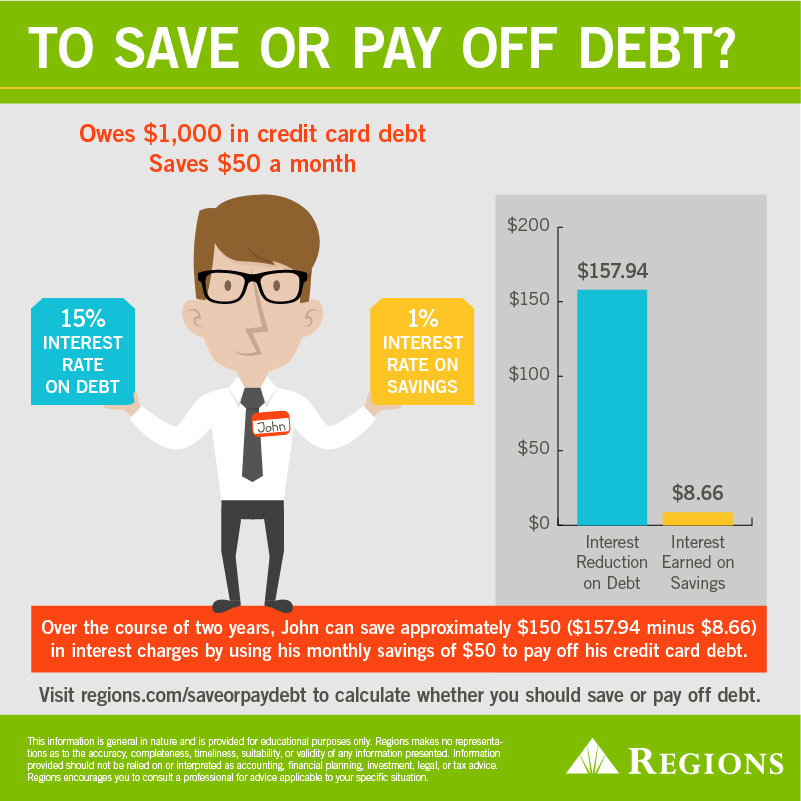

2. How much does your debt cost you?

If you have money in a rainy-day fund, it may make sense to focus extra cash on debt repayment. Most savings accounts earn a small amount of interest per year, while credit card issuers regularly charge more than 15 percent interest per year.

To calculate your own debt burden, make a list of all your monthly obligations (car loan, mortgage, credit card debt, etc.) and the interest rates of each. Multiply the balance by the interest rate for each obligation, and add up the results. This provides an idea of how much your debt costs you per year.

Use the "Save or Pay Off Debt?" calculator to compare the financial return you'd realize from saving versus from paying off debt. If you can save more by putting extra money toward paying down debt than you can earn by putting it toward savings, paying off debt can be a savvy decision.

3. What are your financial goals?

If you have big goals, such as buying a house, saving for your kids' education, or retiring abroad, you'll likely need long-term savings to achieve them. In that case, you might infuse your savings account with extra cash when you can, above and beyond the money in your emergency fund.

Of course, paying off debt can be equally advantageous for big goals. For example, even if you've saved for a down payment, a negative balance sheet can hinder your ability to get a mortgage. Plus, eliminating debt can allow you to funnel more money toward financial goals, which you may be able to achieve more quickly as a result.

4. Can you cut your expenses?

If you have enough extra money for only one financial objective, finding creative ways to make and save money can yield enough cash to fund a mix of all three. For example, selling unused items online, getting a part-time job on the weekends, or finding a cheaper cell phone plan can provide you with extra money each month to put toward your emergency fund, long-term savings, and debt repayment. It doesn't have to be one or the other. With enough creativity and discipline, it can be all of the above.

When you find yourself with some disposable income, there's no universal right or wrong answer for what to do with it. By asking yourself these four questions, you can determine which path makes the most sense for you.

Related Insights

-

Article

Article

-

Calculator

Calculator