Economy Commentary

The Economy

U.S. Economy Resilient, But Not Immune . . .

June 2026

The U.S. economy has proven to be more resilient than many would have anticipated in early March, at the start of the conflict with Iran. Consumer spending has held its own, business investment spending continues to grow at a robust pace, conditions in the manufacturing sector continue to improve, and the labor market seems to be on firmer footing than it was earlier in the year. To be sure, the housing market remains a glaring weakness, particularly with the increase in mortgage interest rates seen since the start of the conflict. Moreover, inflation has reaccelerated, and while the obvious catalyst is the spike in energy prices that have pushed headline inflation meaningfully higher, the reality is that by their own preferred measure, core inflation has been above the FOMC’s 2.0 percent target for five straight months.

Perhaps the changes in economic conditions and perceptions of the U.S. economy are best captured in the dramatic change in expectations for the path of the Fed funds rate. Earlier this year, analysts and market participants were debating how many times the FOMC would cut the Fed funds rate as they rode to the rescue of the labor market. By the end of the first week of June, that debate had shifted to how many times the FOMC would hike the Fed funds rate to help quell stubborn inflation pressures. Still, just as we sat out the debate earlier in the year, we’re sitting out the current debate. We came into this year thinking there was very little room for the FOMC to move, and we think that remains the case despite the world around us looking very different than it did at the start of 2026.

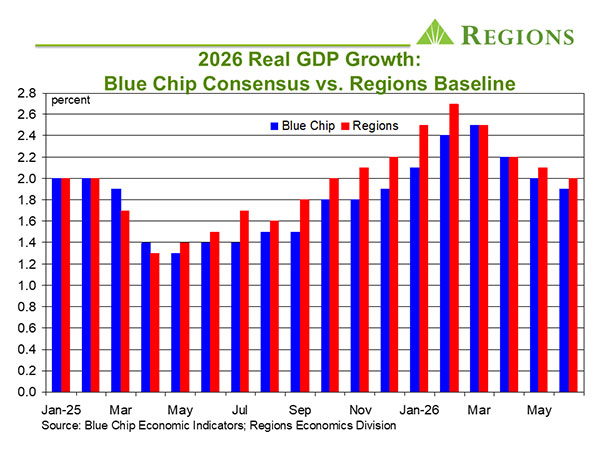

To say the economy has been resilient in the face of jumps in energy prices and interest rates since the start of the conflict is not to say the economy has been immune. In particular, higher prices have weighed on real growth, as we discussed in last month’s edition. One way to see this is to trace the path of our baseline forecasts of 2026 GDP growth over the past several months. Since our February forecast of 2.7 percent growth, our forecast of full-year 2026 real GDP growth has come down in each successive month and, as of our June forecast, stands at 2.0 percent. As our forecasts of real GDP growth have been marked down, our forecasts of nominal GDP growth have been marked steadily higher, the divergence reflecting the extent to which our inflation forecasts have been revised higher.

Simply stated, higher prices mean that each additional dollar of spending at current prices translates into a smaller increase in spending after adjusting for prices, i.e., real spending. One way to think of it is having to run faster and faster (nominal spending) just to stay in the same place (real spending). Thus far, consumers have been able to spend at the faster pace dictated by rising prices thanks to a number of supports. One is that aggregate labor earnings, the largest block of personal income, continue to grow at a rate faster than inflation. Consumers have also benefitted from meaningfully larger income tax refunds this year than those seen last year, while continued increases in equity prices have helped sustain the wealth effects that are supporting spending amongst upper income households. Additionally, a steadily declining saving rate suggests consumers are dipping into savings to help keep pace with rising prices.

Still, there is cause for concern. The cushion from income tax refunds is being rapidly pared down and consumers could easily reach the point where they’re inclined to cut back on spending rather than further deplete savings. At the same time, faster inflation means the gap between growth in labor earnings and inflation is much narrower at present than had been the case, meaning less support for real spending growth. That support would be further weakened by a deterioration in labor market conditions. Concerns over the labor market, however, have abated considerably, in stark contrast to earlier this year. It is striking that while earlier this year many were pointing to the labor market as grounds for the FOMC to make further cuts to the Fed funds rate, in the wake of the May employment report many are now pointing to the labor market as giving the FOMC the latitude to raise the funds rate to combat stubborn inflation pressures.

Total nonfarm payrolls rose by 172,000 jobs in May, more than double the consensus forecast, with private sector payrolls up by 120,000 jobs and public sector payrolls up by 52,000 jobs. At the same time, prior estimates of job growth in March and April were revised upward by a net 93,000 jobs for the two-month period, and the unemployment rate held at 4.3 percent. In the wake of the release of the report, yields on U.S. Treasuries moved higher across the entire yield curve, and a 25-basis point increase in the Fed funds rate by year-end was more than fully priced into the futures market, a reaction which we find more than a bit baffling. Indeed, our take on the May employment report, and the reaction to it, is that seldom have we seen so much made out of so little.

The details of the data support our take. May’s increase in public sector payrolls was driven by payrolls in local government excluding education rising by 43,500 jobs, while the increase in private sector payrolls was driven by payrolls in leisure and hospitality services rising by 70,000 jobs. What the two have in common is that they were largely driven by hiring ahead of the World Cup, with local governments taking on workers to help with things such security and infrastructure and businesses, particularly restaurants, adding staff in anticipation of higher customer traffic. To the extent this was the case, it follows that once the World Cup is over, payrolls in these segments will go back to where they would have otherwise been. In addition to the outsized increase in payrolls in leisure and hospitality services, healthcare payrolls rose by 47,200 jobs in May, with these two segments almost fully accounting for the increase in private sector payrolls.

All but lost in the hype over the headline job growth numbers over the past few months is that, despite the big headline prints, there has been strikingly little growth in aggregate private sector hours worked, which is what matters for output growth. To that point, despite the gain of 120,000 jobs, aggregate private sector hours were basically flat in May. In part, this is compositional, as job gains were concentrated in leisure and hospitality services and health care, industry groups in which weekly hours are well below the private sector average. That aggregate hours were flat means that the sizable increase in private sector payrolls did little to advance output growth in May while also blunting the increase in aggregate private sector wage and salary earnings.

Gains in household employment over the past several months have lagged gains in payroll employment by a wide margin, and that the unemployment rate has been basically flat is a testament to how tepid growth in the labor force has been. To some extent, this reflects the ongoing decline in the foreign born labor force, which we’ve been pointing to since late-2024 as a potentially powerful drag on job growth. Additionally, even though the layoff rate remains below pre-pandemic norms, those who do lose a job are having a harder time finding another, which is reflected in the rising duration of unemployment and what, excluding the pandemic period, is now the highest level of long-term unemployment (27 weeks or more) since 2016.

Our view of the labor market has not changed for quite some time. Just as earlier in the year we were pushing back on the dour takes on labor market conditions, we now find ourselves pushing back on the narrative that the labor market is again firing on all cylinders. We’ve consistently pointed to supply side and demand side factors holding down job growth and have argued that what will be notably slow trend job growth will nonetheless be sufficient to keep the unemployment rate stable if not slightly lower. If and when we have grounds to change our view, we will, but the May employment report doesn’t come close to warranting that, let alone providing a rationale for the FOMC to hike the Fed funds rate.

While such a move may come at some point, it won’t come at this month’s FOMC meeting. As noted above, as measured by the PCE Deflator, core inflation has been at least one hundred basis points above the FOMC’s 2.0 percent target rate for five straight months (the May data will make that six straight months). Moreover, indicators of early-stage price pressures, such as the Producer Price Index, show intensifying upward pressures on costs for producing and shipping goods that figure to, at least in part, ultimately show up in measures of core inflation on the consumer level. Clearly, there will be no “easing in” period for new Fed Chair Warsh but, that said, the only “news” likely to come out of this month’s FOMC meeting is the Committee dropping the implicit easing bias from their post-meeting policy statement, a move that seems well overdue.

Sources: Bureau of Economic Analysis; Bureau of Labor Statistics; U.S. Census Bureau

As of June 10, 2026

Related Insights

-

Article

6 min read

Article

6 min read

-

Article

11 min read

-

Article

12 min read