What association health plans mean for small businesses

Many small-business owners and their employees have struggled to find affordable health care and are looking for an alternative. AHPs might offer a solution.

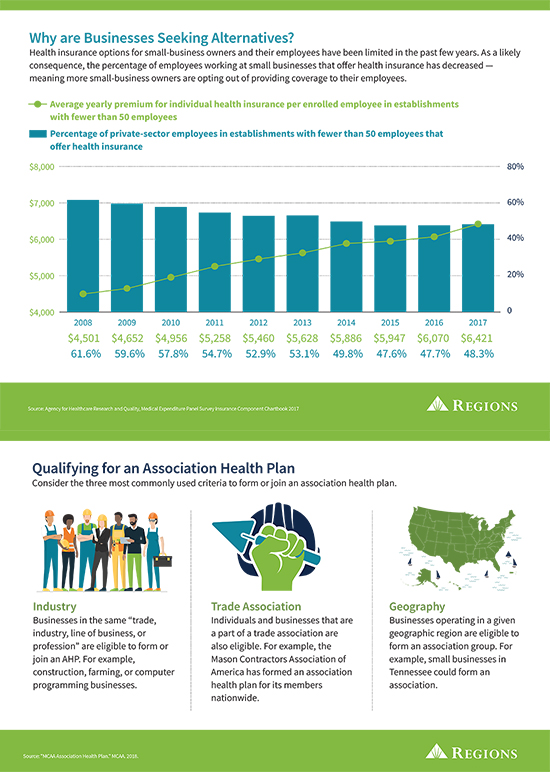

Small-business owners face many challenges — from managing cash flow to retaining talent to meeting customer needs. In recent years, 80 percent of owners have had another concern: the cost of health insurance, according to an eHealth survey. With many employers looking for alternatives to traditional health insurance plans, a new option is coming into play — Association Health Plans (AHPs).

AHPs: A solution for small-business owners?

Association Health Plans aren’t a totally new concept, but in the past, they were restricted to those working in specific industries and employees belonging to trade associations. Groups of people (associations) would band together so they had more leverage to negotiate lower premiums so they could reduce health care insurance costs. This allowed small-business owners to offer benefits comparable with larger companies, without breaking their bottom lines. The problem was that most employers weren’t eligible to join an AHP because they were only open to a strict subset of industries.

These restrictions were loosened starting in 2018: The U.S. Department of Labor announced a new rule that made AHPs available to a broader pool of small businesses. This was on the heels of an executive order from President Donald Trump intended to confront rising premium costs. According to the Department of Labor, “AHPs allow small employers to band together to purchase the types of coverage that are available to large employers, which can be less expensive and better tailored to the needs of their employees.”

Eligibility requirements

Let’s take a closer look at the new, expanded rules to help you get a sense of whether your small business might qualify.

The biggest rule change is expanded criteria for which businesses can band together to form a new AHP or join an existing AHP. Members must be in the same “trade, industry, line of business, or profession.” For example, a small shipping and logistics business could, under the new rule, band together with similar businesses in its line of work. Previously, strict requirements dictated which employers were eligible and which were not.

The second big change is location based: Employers operating in the same region can now form an AHP on the basis of their geographic proximity, including regions that cross state lines.

Another important change is that members can form an association for the sole purpose of providing employees with insurance through the AHP. Specific requirements vary by state, but your small business might be eligible to form an AHP by joining together with other businesses in your industry or geographic area.

The benefits of AHPs

For small-business owners, the primary benefit of an AHP is that it can help you strengthen your bargaining position with insurance companies, which could lead to more cost-effective plans and a greater variety of insurance options. When you join an association, you negotiate as though you’re a single large employer. That could help you reduce health care insurance costs because you have strength in numbers, and the economy of scale that comes with it.

The new AHP rules include many of the same consumer protections and anti-discrimination protections mandated by the Affordable Care Act, such as the requirement to cover employees with pre-existing conditions. AHPs must also cover preventive care for employees and cannot cap lifetime or annual coverage. However, new Department of Labor regulations allow for key differences, including that companies with 50 or fewer employees do not have to cover all of the essential benefits in the ACA, such as maternity, mental health, prescription drug coverage, and rehab.

It’s too soon for dollar estimates around how much AHPs can potentially save your business, but experts believe looser restrictions and collective bargaining may help small businesses cut health insurance costs.

Potential drawbacks of AHPs

Before joining an AHP, consider some of the potential drawbacks. For instance, association health plan costs can vary greatly depending on your employee pool and industry.

AHPs can charge employers different rates based on gender, age, and location of their employees because of perceived cost and risk. If a health insurer believes your employees will be expensive to insure or your line of work is risky, they will likely charge you more. Consider a company that employs older workers in manual labor that puts them at risk of chronic injury. That company is likely to face a higher premium than a company employing younger workers to do desk jobs, even through an AHP.

Similarly, a recent study by the Blue Cross Blue Shield Association estimated that AHP premiums for women in their early 30s might be more than 30 percent higher than for regular individual and small groups, presumably because of the potential maternity care costs. Meanwhile, the same study estimated AHP premiums for men in their 30s could be more than 40 percent lower than ACA rates.

Be sure to consider how your industry and your workforce might affect your rate under an AHP. Generally, companies with younger, healthy workers are likely to benefit from AHPs, while those with older workers might not reap the same savings.

There are also additional costs associated with switching to a new health insurance plan. While you may save money in the long run, you need to be sure to have the cash flow to cover a switch, as well as the time to explore the array of new plans available through an AHP.

One final word of caution: the new AHP rules were implemented by an executive order, meaning that they’re not set in stone. Plus, attorneys general in 12 states have filed a lawsuit challenging the new rules, so it is possible that this order could be changed or reversed.

Related Insights

-

Article

7 min read

Article

7 min read

-

Article

5 min read

-

Article

9 min read

-

Article

4 min read