Have you disaster-proofed your business?

Planning to overcome your greatest risks could help your business achieve its highest potential.

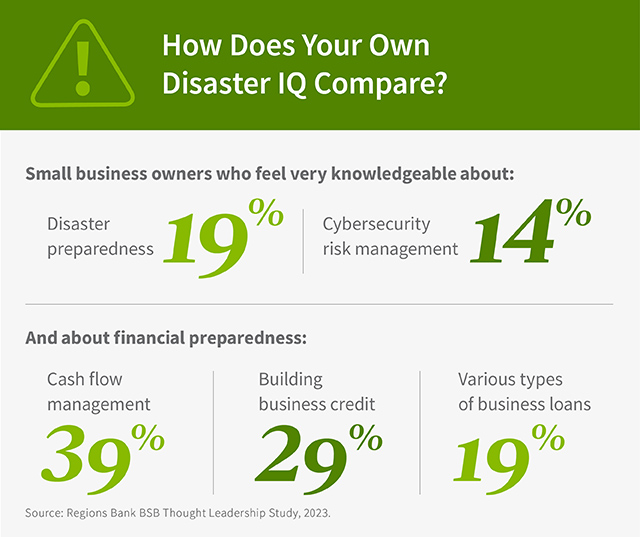

Amid all the challenges of running your business, preparing for what-if disasters may feel like a distraction or needless expense. Research indicates that many owners prefer to focus their attention elsewhere. According to a 2023 survey by Regions Bank, just 19% of small business owners describe themselves as very knowledgeable about how to prepare for disasters.

Yet virtually every business faces seen and unseen risks, says Charles “Chuck” Self, Head of Business Resilience for Regions Bank. Hurricanes, floods and other natural disasters cost U.S. businesses billions in damage and lost output each year, and a quarter of affected businesses never reopen. Nor are such incidents as rare as they may seem: More than 10% of small businesses in one survey reported revenue losses due to a natural disaster just within the last 12 months.

Beyond natural disasters, the COVID pandemic provided stark evidence of how health crises can arise from nowhere, shutter many businesses and force others to reinvent operations overnight. Cybercrime, meanwhile, can cost small businesses significant money. Yet the Regions study showed that just 14% of owners feel prepared for cyber risks.

While routine setbacks and disruptions are a normal part of business, “a disaster is something different. It typically comes on without warning, forces you to turn on a dime and threatens on a very large scale your ability to serve customers,” says Self. “So unlike with regular business planning, preparing for disaster is specialized and demanding.”

Assess and address the risks

To prioritize preparation and response planning for potential disasters, start by focusing not on each potential type of disaster, but on the areas of your own business and the places where you might be most vulnerable, Self advises.

For most, that comes down to three main risks: operational, financial and regulatory.

Operational risks. “Think about events that could shut down your factory or data system,” Self advises. While floods, tornadoes and cyberattacks may each call for specific insurance, infrastructure or response preparation, starting with an overall look at your operations can help you uncover and address your greatest vulnerabilities.

For example, if all or most of your production takes place in a single facility, having a provisional second plant in a different location could help you get through the worst of the crisis if the first plant is disabled. Likewise, what cloud or other backup do you have for your data, to ensure access to the information you need if your main systems are breached? What are your alternate sources of power in case the electrical grid in your area goes down?

And it’s not just your own operations you need to worry about, Self notes. The COVID pandemic exposed supply chain weaknesses that are still reverberating through the U.S. and global economies. Carefully review your own suppliers and providers, Self suggests. Ask about their financial health and what their disaster plans look like. If your ability to operate depends on one supplier, or suppliers from a single country or region, look for ways to cultivate backup suppliers, especially ones located closer to where you operate.

Financial risk. When disaster strikes, survival often depends on reliable access to cash to continue to keep the lights on, purchase the supplies you need, make repairs and pay your employees. It’s easy to take cash flow for granted during good times, and the Regions study found that just 39% of owners feel very knowledgeable on the subject. Just 29% felt the same about building business credit, and fewer still (19%), felt very knowledgeable on business loans.

Now may be a good time to review your cash flow with your Regions advisor, to consider how you’d keep it going during an emergency, Self suggests. For example, you might consider opening a line of credit that you would only tap when needed. Another key, of course, is to speak regularly with your insurance specialists to make sure you’ve got the coverage you need for different types of emergencies.

Your greatest financial vulnerabilities may lie in areas of concentrated risk. “If too much of your capital is devoted to a single investment, your advisor could help you consider ways to diversify,” Self says. As with your supply chain, consider your customer list. How healthy are their own operations? What would the impact on your business be if your largest customer suffered a setback, or changed course and stopped buying? Look for ways to expand your list.

Regulatory risk. As a business owner, you know that regulation has been on the rise. In addition to those applying to your sector, businesses of all types are being held to new and stricter environmental impact standards, workplace regulations and more. “Thoroughly review the various regulations you face, and make sure you’ve hardened yourself against those,” Self says.

Develop a disaster response plan

No matter how thorough your risk review and preparation are, disasters come unexpectedly and contain surprises. “Once you catalog your risks, the next step is to develop business resilience plans that allow you to respond quickly and continue operating,” Self says.

“The very first step is always to make sure that your employees are safe and well,” he adds. In case of a physical disaster, be sure you’ve got a well-thought-out evacuation plan for your facility, and that all of your workers have practiced it. For your physical plant, make sure people are assigned to tasks such as turning off equipment and power, in case of a weather-related disaster.

“Another top item for your checklist is contact information for your key players and the leaders, and a communication plan,” Self says. That communication plan should include your key suppliers and customers, as well as your Regions advisor, insurance specialists, attorneys and other experts. And ensure that your financial records are protected and easily accessible during any emergency.

Practice and update

“Just having a plan and checklist isn’t enough,” says Self. Practice your emergency response with your key people regularly and ensure all employees understand what their first steps should be. And keep in mind that conditions continually evolve; review and update your plan at least once a year, he suggests.

While these steps certainly require an investment of time and capital, that investment could more than pay off by enabling you to protect employees and continue operating through the worst of a crisis and build back quicker when it’s over. The best part, Self adds, is that even in the happy event that your business remains disaster-free, the very act of planning and preparing can make your business stronger, tougher, more adaptable and better able to meet whatever challenges and opportunities come your way.

Three things to do

- If you have been impacted by a disaster, consider your next steps.

- Review this checklist to ensure you are prepared for any disaster.

- Bookmark this list of disaster recovery links and our Disaster Resource Center.

Related Insights

-

Article

7 min read

Article

7 min read

-

Article

6 min read

-

Article

4 min read

-

Article

5 min read