How to build generational wealth

A comprehensive guide to creating generational wealth, improving your family’s money mindset, growing your legacy, and ensuring it’s maintained for generations to come.

Sometimes referred to as family wealth, generational wealth commonly refers to financial assets that are passed down between generations such as cash, real estate, stocks, life insurance, or a family business.

While the term might conjure up thoughts of trust funds and immense privilege, the true definition of generational wealth encompasses far more than just tangible assets. “It’s creating and leaving a legacy that provides for your children — not just about passing on a lump sum of money, but educating them and giving them the tools to thrive and create their own legacy,” says Rachel Tatum, a Financial Advisor for Regions Investment Solutions.

Whether you’re starting with $1 million or $1,000, creating generational wealth is an achievable goal, but one that will require a careful plan that’s tailored to both your goals and your unique financial situation.

- For families of means and high-income households: Generational wealth may be easier to build, but more difficult to maintain. Careful estate planning and thoughtful conversations about money will be essential to ensuring your legacy withstands the next generation. According to research firm Cerulli Associates, $124 trillion in wealth is set to change hands through 2048.1 More than half of those funds are expected to come from high-net-worth and ultra-high-net-worth households.1

- If you’re just starting out or have less expendable income: While creating generational wealth can be more of a challenge for the average American family, the right strategy can help make that dream a reality at any income level. Careful planning and know-how will be key to helping you create a lasting legacy.

In this article, we’ll discuss:

- How to create generational wealth

- Strategies for maintaining generational wealth

- Tips for establishing a positive money mindset

- How to raise financially confident kids

How to build generational wealth

When it comes to creating generational wealth, one of the most common misconceptions is that it’s simply not feasible for the average American. “It’s very feasible. Anyone can create generational wealth,” Tatum says.

Regardless of whether you’re just starting out or are well on your way to achieving your goals, the key is to start with a strong financial plan. As you create your plan for building generational wealth, consider the following tips.

Balance debt vs. savings

Your plan should go one step further than a standard household budget, focusing on strategies that allow you to pay down debt while increasing your savings. Tatum advises her clients to incorporate their retirement savings as a line item in their budget. “Whatever is left over can then be used for other goals, such as college savings or investing,” she explains.

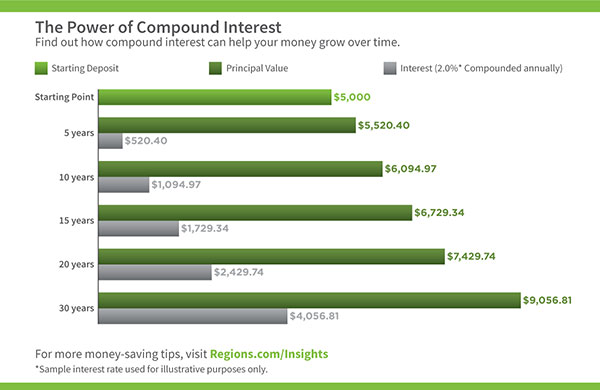

Leverage the power of compound interest

For many, knowing how to start investing can be a challenge. As a financial advisor, Tatum sees many clients struggle to overcome the idea that they don’t have enough money to invest. “Everybody has to start somewhere. There's not a dollar amount that dictates whether you should or shouldn't invest,” she explains. “You can start with as little as $50 a month, and it will grow over time thanks to compound interest.”

Consider life insurance

Life insurance can be used for much more than simply covering your final expenses. Whole life insurance pays a benefit upon the death of the insured while also accumulating cash value, serving as a form of inheritance.

Think about opening a 529 Plan

Given the long-term impact of student loan debt, opening a 529 Plan and saving for your child’s education can be an effective way to support their financial future. “If your child is able to come out of college without any student loans, that’s significant. They can focus on starting their career, saving for their first house, and start saving for retirement at a very early age,” Tatum says.

As you grow, grow your wealth

“As you get raises, increase your retirement contribution. If it's money that you weren't seeing before, you can be OK with not seeing it. Increase that savings as time goes on,” Tatum advises.

Maintaining generational wealth

For families of means, generational wealth is often easier to grow, but it’s often more difficult to maintain. In fact, studies show that 70% of families lose their wealth by the second generation, and 90% lose it by the third generation.2

“The first generation is the one that makes the money, the second generation is the one that spends it, and the third generation often sees none of that money,” explains Paige Christenberry, a Wealth Advisor at Regions Bank in Knoxville, TN.

Careful planning, thoughtful conversations, and strategic guidance will be essential to ensuring your legacy withstands the next generation. For many families, working with a wealth advisor will be a valuable first step.

“As wealth advisors, we bring in other members of our team to offer advice and guidance on aspects of your estate plan, such as a portfolio manager who manages the actual assets under investment, and a wealth strategist who can come in and create a plan of action. We also work with our clients’ individual estate planning attorneys, and CPAs,” explains Christenberry. “We act as the quarterback of these relationships.”

Safeguard your legacy

Careful estate planning can help ensure that when you transfer your wealth to the next generation, it's done so in the best way possible. For those who aren’t confident in their children’s ability to carefully manage their inheritance, there are a variety of estate planning strategies that can be used to ensure your legacy is maintained.

“There are very creative ways to structure a trust. It's a good way to ensure your family is carrying on your legacy after your passing,” explains Christenberry. Depending on the complexity of your estate, you might also consider appointing a professional executor, particularly if you’re concerned about your heirs’ ability to manage your assets.

Have a positive money mindset

Both Christenberry and Tatum note that one of the most common mistakes people make is failing to talk to their children or grandchildren about money. “Having these discussions, regardless of income level, is critical to maintaining your family’s wealth over time,” explains Christenberry. “You have to be open with your family about assets and intentions. We don't do our families any favors by being secretive and closed off.”

The following actions can help ensure your children or grandchildren are well-prepared to maintain your legacy:

- Involve your family in wealth planning or financial planning discussions

- Document your estate plans and discuss your wishes

- Have frequent discussions about your family’s mindset and values

“Your kids don’t have to know everything about your personal finances, but when you get them involved, they won’t feel like it's something hidden or secretive,” Christenberry said. “When you involve your family, you're letting them know that you trust them.”

How to raise financially confident kids

Financial education is an important, yet commonly overlooked component of generational wealth. By educating your kids on how to plan and save, you're investing in them so that they can become financially fit whenever they grow up.

The following tactics can help you instill the right financial mindset into your kids or grandkids, ensuring they’re well-equipped to maintain your family’s legacy:

- Discuss the value of a dollar. One tactic Christenberry has used with her children is to instill the concept of wants versus needs. “When my son wants to purchase a video game, I explain this is a want and he will have to use his own money that he’s earned to purchase it. I will pay for his needs, such as food, gas or school supplies. He learned quickly that his wants were not as important when he had to use his own money!”

- Save, share, spend. Your kids are never too young to learn how to budget. Discover tips for teaching kids how to manage money.

- Get them invested. “It's important to show your kids what it means to invest and how it benefits them over time,” says Tatum. “I have a lot of clients in their twenties that are afraid of investing because they've never had any experience in it.”

Ultimately, ensuring your children have a positive money mindset is one of the best ways to set them up for lifelong financial success. “If you're helping your child, educating them at an early age and saving for them at an early age, it's not just giving them a silver spoon,” Tatum notes. “It's building their knowledge on how to save, how to budget, and how to grow their own wealth.”

Talk to your Wealth Advisor about:

- Re-evaluating and adjusting your wealth plan annually, or as life circumstances change.

- Ways to engage in careful estate planning and estate plan coordination.

- Teaching your children how to save, invest and plan for the future.

- Involving your family in wealth planning discussions.

Want to get started with wealth planning?

Our wealth management guide can help on your journey to generational wealth.

Interested in talking with an advisor but don’t have one?

Find a contact in your area.

Sources:

1. Cerulli Associates. “Cerulli Anticipates $124 Trillion in Wealth Will Transfer Through 2048,” December 2024.

2. CFA Institute. “How Real Is the Third-Generation Curse, and How Can Financial Advisors Tackle It?” February 2025.

Rachel Tatum

Rachel Tatum is a Financial Advisor for Regions Investment Solutions and a Senior Vice President with more than 20 years of experience.

Paige Christenberry

Paige Christenberry, CFP®, CWS®, CDFA®, is a Wealth Advisor with more than 27 years of experience.

Related Insights

-

Article

16 min read

Article

16 min read

-

Article

14 min read

-

Article

19 min read

-

Article

9 min read