Bridging the gap: Wealth across generations

How generational perspectives may be shaping the future of money.

Baby Boomers (born between 1946 and 1964) often value stability, homeownership and long-term investments, while Generation X (born between 1965 and 1980), who came of age during economic uncertainty and the rise of credit culture, tend to be a bit more pragmatic and debt-conscious.

Breaking from the status quo, Millennials (born between 1981 and 1996) often carried student loan debt and faced rising living costs as they stepped into adulthood. As a result, they often value flexibility and purpose-driven spending.

The youngest generation we explore in this look at money perspectives—the digital natives of Gen Z (born between 1997 and 2012)—have grown up amid rapid technological change and geopolitical unrest. This generation is redefining wealth with a focus on financial independence, side hustles and ethical consumerism.

Work and retirement: Baby Boomers and Generation X

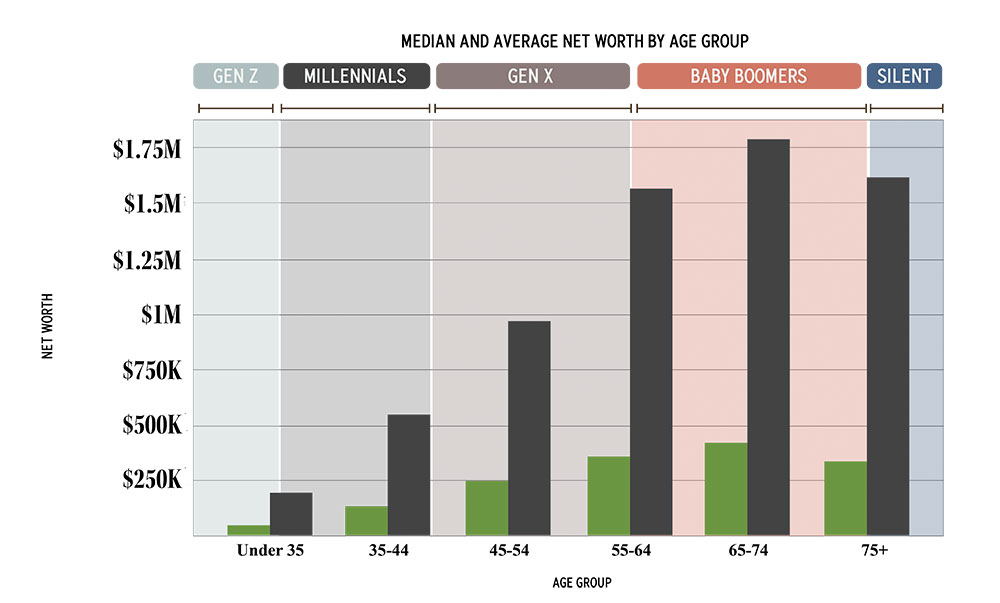

Members of the Baby Boomer generation often worked their entire careers with one company, much like their Silent Generation predecessors. The wealthiest generation, according to Investopedia, Boomers usually bought homes when prices were low, earned comfortable wages, and contributed to employer-sponsored retirement plans just as the stock market began its long bull run, therefore benefiting from decades of rising asset prices.

According to recent Federal Reserve data, Baby Boomers control more than half of all U.S. household wealth, having double that of Generation X and five times that of Millennials.

Transamerica Institute’s Multigenerational Workforce survey notes that Baby Boomers have rewritten societal rules at every stage of life, including retirement. By working into older age and seeking a flexible transition to retirement, they are upending the long-standing notion that work and retirement are mutually exclusive.

The American Society of Pension Professionals and Actuaries refers to the recent study noting many of today’s workers expect to work beyond the traditional retirement age of 65, or they do not plan to retire at all—the majority plan to continue working at least part-time in retirement. Notably, among those planning to extend their working lives, most plan to do so for both financial and healthy aging-related reasons.

Olivia Wiggins, Trust Advisor, works with clients across the generational divide and has noticed this trend. “Gen X—who are getting closer to retirement age—seem to be more focused on retirement, while I see more Baby Boomers working further into the average retirement age.”

Heidi Coombs, Wealth Advisor in Texas, agrees and sees a common thread across generations. “Entrepreneurs are entrepreneurs,” she notes. “Many individuals, as they approach retirement or the sale of their business, have found another entity or project/outlet to channel that energy. It’s how they are wired.”

“Many younger Baby Boomers who are now retiring have seen their parents retire and lose their purpose,” notes Aimee Chester, Wealth Advisor in Texas. “They have seen friends retire and get hit with a life-changing diagnosis. As a result, they value their role and position while recognizing that post-retirement health and well-being is not to be taken for granted.”

Chester also shares a trend of families moving closer to children and grandchildren in order to play a more active role as grandparents–often also seeking to play a larger financial role in their grandchildren’s college future.

Work and retirement: Millennials and Gen Z

Millennials are often credited with redefining the workplace, shifting the focus toward a better balance between work life and personal life. Entering their careers during the Great Recession, they ushered in a different approach, viewing work as a means to an end rather than a core aspect of their identity. In the post-pandemic era, this often looks like remote or hybrid workplaces and flexible schedules. As far as retirement goes, this generation joined the workforce during some economic uncertainty. With the questions around the viability of Social Security, many see themselves working well into retirement age. This is especially true for the 33% who became unemployed during the pandemic.

“When discussing retirement with Millennials, many are aiming to retire at 50. If I were to go back and ask my 35-year-old self, I may have said 50 as well,” notes Chester.

Even when they do retire, they plan to do so with a sense of adventure, intent on keeping up an active lifestyle. This takes smart financial and retirement planning, especially in an uncertain economy. Thankfully, more than 85% of Millennials contribute to an employer-sponsored retirement plan according to the Transamerica Institute survey.

As the youngest generation currently in the workforce, Gen Z has decades ahead to work and plan for retirement. Their neophyte status may be one reason this generation is currently contributing the least to their employer-sponsored retirement plans at 71%. However, as part of an ongoing trend, they began contributing to retirement funds at a much younger age—an unprecedented average of 20 (which is five years earlier than their Millennial counterparts).

Generational stereotypes: Sew it, grow it, blow it?

When talking about generations, one can get caught up in stereotypes. Wiggins notes that when she began her career in wealth management, she was told she would typically see the following trajectory: the first generation makes the money, the second generation saves the money, and the third generation spends the money. This assertion does have some legs and is reflected in the data from studies on family businesses. According to the “three-generation family business rule,” which Family Business United explores in more detail, most family-owned businesses fail or are sold by that third generation.

“While that is not always true,” says Wiggins, “the further a family generation gets from the founders, the less likely it is to see aggressive savings, irrespective of defined generation.”

The Baby Boomer generation or earlier often planted those first seeds of family wealth. They spent years building that wealth through their careers or businesses, at times not seeing the fruits of their labor pay off until they were nearing or in retirement. As a result, their children (Gen X and/or Millennials) did not necessarily grow up with wealth.

These generations often took responsibility for establishing themselves independent of their parents, creating their own financial path. Whether taking over the family business or building careers of their own, they are focused on building their own wealth.

Interestingly, it is this cohort that stands to benefit financially from the coming Great Wealth Transfer. They have earned and saved on their own, while their parents’ (or grandparents’) wealth amassed and is set to be passed along through trusts, real property, and more. These individuals, now in their 30s to late 50s, are positioned to be good stewards of money largely with an intent to continue to build and save wealth for future generations.

One caveat—though rare—seems to span generations: The approach to “die with zero.” A book of the same name, published in 2020, focuses on the premise of living rich rather than dying rich. However, this seems to be more the exception than the norm.

“The majority of individuals and families we work with don’t want to spend their money. They are focused on growing and protecting their wealth for the next generation—creating a financial safety net for their children and grandchildren,” notes Jennifer Wilson, a Trust Advisor in Alabama. “And while we see examples of those adult children and grandchildren embracing this generosity to the fullest, we also see the younger generations seeking to make their own mark by building and creating their own wealth.”

The changing global digital world may have the most influence on Millennials and Gen Z, who have grown up watching not only the Joneses next door, but the Joneses on their various screens. Another defining attribute: These digital natives are often more comfortable with payment apps than with cash and lean more on online shopping than in-person retail therapy. They also put more stock in products and brands they believe in. They tend to be more willing to spend their money on products and services that align with their personal values.

The younger generations: An eagerness to learn

An observation among Wealth Advisors about the younger generations is their eagerness to learn.

“The younger generations generally stayed at home longer and may have been a bit more sheltered than their predecessors. We find, from a financial planning perspective, they want the advice,” notes Wilson. “It is an interesting dynamic with Millennials and Gen Z. They know they can learn it all, but they don’t always trust themselves to know what to do when it comes to managing money and financial planning.”

Elise Carr, a Wealth Advisor in Birmingham, agrees.

“There is a tremendous amount of interest from Millennials and Gen Z in learning proper money management. With increasing inflation, the higher cost of homeownership, and overall cost of living, there is greater interest in saving and learning good money habits early on. I’ve seen a surge in responsibility in spending, as well.”

Generations and money: Influencing money matters

It turns out that an individual’s defined generation may have less influence on their attitudes about money and wealth than the stereotypes would have us believe. The biggest influence on how we view money may lie within our family systems. What the adults in our lives model around finances may be absorbed as we form our individual views—and values. There are certainly the opposing outcomes, where a child may go in the exact opposite direction of their parents when it comes to fiscal focus. But more often than not, we learn and build our own money management approach based on what we see around us.

“Interest in learning, aptitude, and the way someone is raised has a heavy influence on our approach to money—and every family is different,” says Coombs. “Some families have mission statements, and even those who don’t have one written generally project their family mission in how they show up in the world.”

When it comes to influencing how the next generation views money, Coombs says it may be more important for grandparents and parents to show, not tell. And it may be beneficial to bring the various generations to the table for ongoing conversations about what matters most—and how to build that mission into your money management and financial planning.

Whether you are enjoying your retirement years or just starting out in your career, being mindful of the psychology around money can create a healthy perspective on saving, investing, and retirement planning. Having a team of seasoned professionals to help guide your money mission can take some of the stress and unknowns out of financial planning, leaving you more time to enjoy the fruits of your labor.

Talk to your Regions Wealth Advisor about:

- Ways to ensure you pass on your values to the next generation.

- What steps you might consider in setting up a family meeting about legacy planning.

Want to get started with wealth planning?

Take the first step with our wealth management guide.

Interested in talking with an advisor but don’t have one?

Find a wealth advisor in your area.

Related Insights

-

Article

10 min read

Article

10 min read

-

Article

12 min read

-

Article

13 min read