How to prevent check fraud from affecting your business

It’s easy to overlook the age-old threat of check fraud, but it’s a costly mistake for business owners. Take these steps if your company has been targeted.

Paper checks may seem old school, but they are still a common payment method for many businesses—making them a compelling target for criminals.

You might think check fraud would be a thing of the past. But incidents of check washing, mailbox fishing, forgery and other crimes that involve checks remain elevated. In 2024, checks were still the most frequent target in payment fraud, with 63% of U.S. businesses reporting incidents, according to the Association for Financial Professionals payments report.

After the U.S. Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN) issued an alert on mail theft-related check fraud in 2023, a review found $688 million in reported suspicious activity over 6 months. FinCEN discovered that the majority of stolen checks were altered and deposited, with some ending up as a template for counterfeit checks or fraudulently signed and deposited.

Check washing, in which criminals use chemicals to “wash” a check, is a well-known method for committing check fraud. But more sophisticated methods have emerged, says Cathy Powell, Treasury Management Product Manager at Regions Bank. “Now fraudsters are using software to do what’s called check cooking, which is using advanced image editing to meticulously re-create authentic checks. They’re also using AI tools to mimic check stock, signatures, fonts and seals, making it extremely difficult to detect.”

Business checks are often targeted because business accounts generally hold more funds than personal accounts, and it can take longer for the crime to come to light. If you’ve discovered that your business has been impacted by check fraud, it’s important to act quickly and carefully. Here’s how to report check fraud and take steps to protect against it.

How does check fraud occur?

Check fraud can happen in a variety of ways. Mail theft is one common way for criminals to obtain checks for fraudulent purposes. Working alone or via an organized criminal network, these criminals may steal outgoing checks from U.S. Postal Service facilities, blue collection boxes or private mailboxes located in buildings or homes or incoming checks from the offices where they are delivered.

Once stolen, the checks may be altered or used to create counterfeit checks, which are then deposited—typically into a bogus account from which the funds are withdrawn before the fraud is ever detected.

- Altered checks: Criminals may take a check and change the recipient's name and/or the amount on a check, often using a process sometimes called “check washing,” which uses chemicals to remove the original information from the check.

- Counterfeit checks: Criminals may use a stolen check to create fraudulent checks. Using the information on the stolen check—including the authorized signature, account number, routing and transit numbers—they can create counterfeit checks that look like they were issued by the same company that issued the original check. Today’s technology has made it easier than ever to create realistic-looking fraudulent checks.

Fraud committed by employees

In some instances, the check fraud may be committed by an employee. Even a trusted, long-time employee who has access to the company’s accounts may turn to check fraud after a tragedy or financial crisis occurs in their personal life.

Unfortunately, if a company doesn't have solid internal controls in place to review outgoing and incoming payments, internal check fraud can be hard to detect—and it may go on for a while.

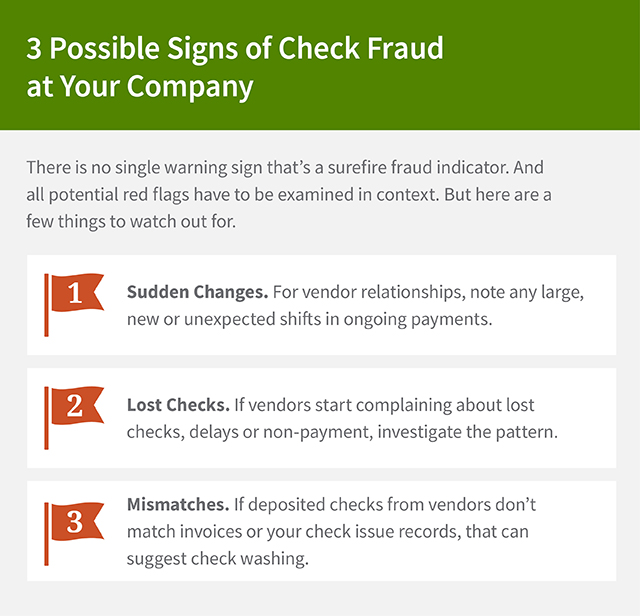

Investigating check fraud

If your company has been affected by check fraud, it’s important to act quickly, carefully and with discretion. First, check your accounts to make sure other instances of fraud haven’t occurred. If you find other discrepancies, make sure to keep a record of all transactions. As soon as possible, report the fraud to your banker. The sooner you tell the bank, the better the bank can help stop the fraud.

Depending on the scale of the loss, you may also wish to contact local police. In some cases, financial institutions—like Regions—will assist the local law enforcement in its investigation. To help with the investigation, you’ll need to identify the recipient’s name and the amount on the original check. You may want to obtain an image of the fraudulent check from your bank and provide it to law enforcement.

Because it’s possible an employee may have been involved in the fraud, it’s important to limit who you tell about the incident. Do not confront, question or alert any suspected perpetrators—doing so may ultimately impede the success of the investigation.

How to safeguard against check fraud

Implementing or correcting processes in your organization can help protect your company against check fraud. Take a hard look at your internal processes and identify areas for improvement. Consider starting with these steps:

- Review transactions. Use online banking to review daily transaction activity and check for irregularities, reconciling outstanding items. Set up automated alerts on account activity. These steps can help your company identify fraud quickly.

- Add checks and balances. Make sure that employees who are authorized to sign checks are not the same people who reconcile the accounts. You may consider instituting two-person authorization on outgoing checks and payments, called dual control. Use Positive Pay services.

- Audit. Conduct surprise account audits on a periodic basis.

- Go digital. Opt for electronic payments over physical checks whenever possible. Solutions like Regions CashFlowIQ can help.

- Avoid using mailboxes. Mailing checks inside the post office (rather than leaving them in mailboxes) offers greater protection against the risk of stolen checks.

Finally, know that awareness can be one of the best lines of defense against fraud. Experts say it’s crucial to make sure your employees undergo a fraud training program.

“Employees are a critical part of efforts to prevent fraud,” Powell says. “They should be trained to recognize and report phishing attempts as well as to verify payment requests, especially those received as ‘urgent’ or from executive impersonators.”

In addition to your internal processes, take advantage of external procedures or treasury management products at your bank that can help you prevent payment fraud. For example, Regions Positive Pay service compares and verifies each check your business issues to the checks presented for payment against your account. The offering verifies the amount, the check number and, as an option, the recipient’s name. Any discrepancies will be reported to you for review.

Even if check fraud has already affected your business, taking time to improve your processes and help combat check fraud can help protect your company from a future loss. For more tips on how to protect your business against fraud, visit regions.com/fraud-prevention/business-fraud.

Next steps:

- Review these best practices for preventing paper-based fraud.

- Use technology to detect and help prevent check fraud. For example, consider Regions Positive Pay or a secure digital payment solution.

- Consider whether you also need to protect against fraudulent ACH debits, which sometimes are called electronic checks. For example, explore Regions ACH Positive Pay.

Related Insights

-

Article

8 min read

Article

8 min read

-

Article

12 min read

-

Article

8 min read