A new era for utilities

Utilities are evolving from income stability to growth opportunity in an electrified, data-driven world.

In a world where energy needs are increasing and electricity demand is growing for the first time in two decades, the Utility sector has gone from being an area of the market where investors simply sought defensive stability and steady dividends to one that is often looked at as a potential beneficiary of electrification and data center growth. With the need for compute growing exponentially, power demand is growing, and the utility sector is at the forefront of this phenomenon. In this piece we will examine the risks and opportunities associated with this new era for utilities and what it could mean for investors.

A resumption in growth for electricity

After the war, power usage grew rapidly in the 1950s and beyond as neighborhoods were formed and household appliances grew in popularity. By the 1980s and the 1990s, computers were a part of many households, and demand for electricity continued to grow. From 2000 to 2020, however, demand was comparatively flat as greater efficiency became the norm.

While demand for electricity was initially driven by lights and motors, increasingly more of the demand now comes from computers and microprocessors, and that need is accelerating at a rapid pace now that data centers are coming into the picture. The utility companies are raising their growth rates as demand has accelerated over the last few years, fueled largely by demand for compute and an increase in onshoring, a theme we have written about in years past.

While the Utilities sector alone is only 2.3% of the market cap of the S&P 500, its constituents are tied into the growth driving the market within two other large top-performing sectors, Technology and Industrials. These sectors are meaningfully linked through power, equipment and compute demand.

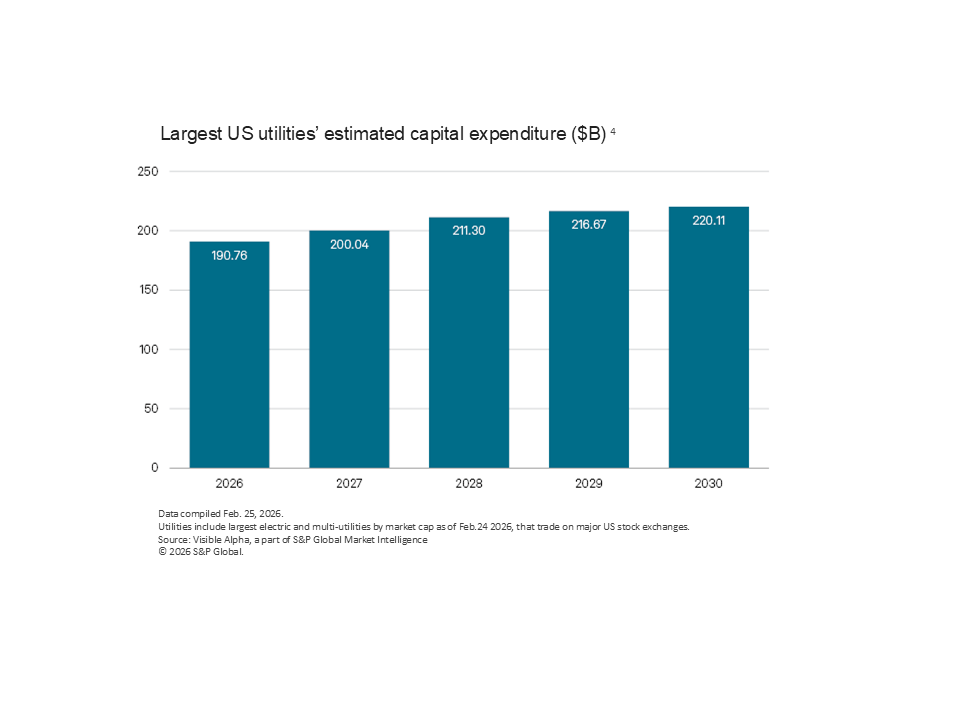

Data center buildout

The hyperscalers are spending hundreds of billions of dollars to advance the growth of data centers and compute to fuel their AI ambitions, and the utility companies and the industrial companies are seeing increased demand for their products and services because of it. Utilities are regulated and the prices that they set for their clients’ utility bills are controlled, so while there is great deal of concern over the impact these data centers will have on household power bills, a few utilities here in the Southeast have actually capped their rates for at least a few years. The utility companies have large capex plans (see Figure 1), however, so funding needs are in focus. We are observing a greater issuance of debt and equity in this dynamic environment, as well as private credit demand. This will bear watching.

An increase in capital market activity

On May 19, 2026 NextEra (NEE), the largest publicly-traded regulated utility company, made an all-stock offer for Dominion (D), the 6th largest regulated utility company. This puts the focus on the possibility of not only these two joining forces on the east coast and in the southeast, but also on the potential for further mergers among utility companies in the months and years to come. The rationale for the current merger appears to be the ability of the acquiror to apply its business model to a company that has struggled a bit, despite being in favorable regulatory environments with great exposure to data centers. It is uncertain as to whether any other mergers of equals will appear in the next year to compete with this one, and the regulatory approval process may be lengthy and could face meaningful uncertainty. We do believe that the merger draws attention to the dynamic nature of this once-staid sector. The world is changing and utilities are changing right along with it.

As more and more demand for electricity arises, companies are seeking alternative uses of energy such as nuclear. While Southern Company’s Vogtle unit is the most recent example of a large nuclear facility (with cost and time overruns that give other companies pause), smaller nuclear reactors are getting more and more attention. This is another part of the puzzle that bears watching.

Conclusion

With two of the largest utility stocks in a holding pattern over the next year or so as a merger is reviewed, the small sector’s price movements may be tied to this deal. Under the surface, however, there are clearly growth opportunities that were not seen for the last few decades within the utility space, and with the strong balance sheets and stable dividends that the large publicly-traded utility stocks have to offer, we continue to believe this is a sector worth watching. Risks of an AI overbuild are a possibility over time, but for the time being, the energy needs are real and so are the higher earnings growth rates that the utility companies are reporting. As long as the balance sheets and the dividend payouts remain stable with their historical levels, we believe that investors will give utility companies the benefit of the doubt with respect to their growth outlooks. The sector has lagged the broader market and is reasonably valued, so despite the hype around hyperscalers and data centers, the sector is still a stable and defensive part of the overall market.

Talk to your Regions Wealth Advisor about:

- Your preferences for regular meetings about your portfolio.

- How to receive Regions Asset Management weekly market commentary.

Related Insights

-

Article

15 min read

Article

15 min read

-

Article

9 min read

-

Article

9 min read