Bonds Commentary

Bonds: Shift In Fed Communications Strategy To Contribute To A More Volatile Rate Backdrop

July 2026

Bonds across segments and of varying credit quality benefitted from the drop in yields on longer-dated U.S. Treasuries during June, with the Bloomberg Aggregate, Bloomberg U.S. Corporate, and Bloomberg U.S. Corporate High Yield index all generating gains of around 0.2% during the month. Credit spreads on high-yield corporate bonds finished the month higher by 8-basis points (bps), while investment-grade spreads leaked wider by just 2-basis points. Yields on U.S. Treasuries maturing inside of 5 years rose during the month as market participants bet on rate hikes out of the Federal Open Market Committee (FOMC) before year-end. All told, the 2-year U.S. Treasury yield rose 16-bps over the balance of the month, while the closely watched 10-year yield finished the month lower by 1-bp.

The flattening of the yield curve was driven by a combination of factors, but chief among them were comments made by new Fed Chair Kevin Warsh following the June FOMC meeting that were perceived to be decidedly hawkish, which put upward pressure on short-dated yields, while falling energy prices and inflation expectations served to pull yields on longer-term bonds modestly lower. Warsh’s post-meeting remarks also included an announcement that he was forming five new tasks forces, with one focused on Fed communications. Mr. Warsh has long maintained a view that the FOMC has been overcommunicating, and his decision to not contribute to the FOMC’s latest Summary of Economic Projections was taken by market participants to imply the “dot plot” could be extinct in relatively short order. Interest rate volatility returned in the wake of Warch’s remarks as market participants priced in the prospect of less hand holding out of the central bank moving forward, and a more volatile backdrop for rates could be a byproduct of any shift in communication strategy as market participants are forced to recalibrate expectations on the fly given limited forward guidance.

Amid this potential backdrop, a broadly diversified fixed-income portfolio remains preferable, with exposures to higher quality Treasuries and investment-grade corporate bonds, high-yield credit, and foreign developed and emerging market bonds all potentially valuable exposures. Bouts of elevated volatility should be expected as market participants are likely to occasionally be caught offside by shifts in Fed policy, which will create dislocations and cause bond prices to diverge from fundamentals more often than we have grown accustomed to. These divergences should present more opportunities for active managers to add value and deliver alpha over time, but in the near term most fixed income sub-asset classes still appear fairly to fully valued, which leaves us with allocations that fall in line with our strategic long-term target exposures as we kick off the 3rd quarter.

High Yield Credit Spreads Leak Wider In June As Demand Can’t Keep Up With Supply. Prices of below-investment-grade bonds moved modestly lower in June as the option-adjusted spread for the Bloomberg U.S. Corporate High Yield index went from 257 basis points (bps) over Treasuries to 270 bps by month end. That incremental move wider comes after index spreads tightened in each of the prior two months from their March peak. From our perspective, more interesting than the absolute level of spreads is the intra-month trend which entailed a series of higher highs for spreads as riskier assets encountered pockets of volatility.

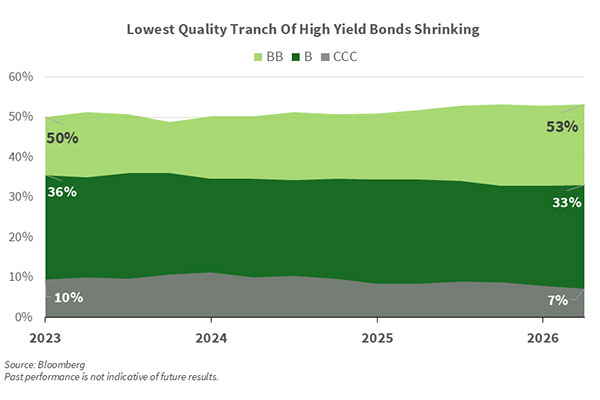

Waning risk appetite played a part in the June pullback in high-yield bonds, but so did the technical backdrop as roughly $34.4B of new paper was issued during the month, the second highest month for issuance this year. All while light summer trading volume led to sparse demand and likely had a hand in pushing bond prices lower. The recent dip in demand could provide a more constructive entry point as underlying credit fundamentals continue to improve with BB-rated exposure climbing to over 53% within the index, while lower quality CCC-rated bonds have declined to roughly 7% at the end of June. All told, the asset class provides ample yield to support prices beyond a modest dip but rising tech exposure in this segment is a potential risk worth monitoring.

As of July 10, 2026

Related Insights

-

Article

10 min read

Article

10 min read

-

Article

-

Article