Can private credit and traditional banking coexist?

Private credit is a rapidly growing asset class that offers meaningful economic benefits by providing long-term financing to companies that are too risky for banks, yet too small for commercial banks or public debt markets. Since the Great Financial Crisis, private credit has become a direct competitor with traditional bank lending. However, the shift of credit from regulated banks and transparent public markets to the more opaque realm of private credit introduces potential risks and rewards for both borrowers and investors. Institutional investors such as pension funds, insurance companies, family offices, sovereign wealth funds, and high-net-worth individuals tend to be the largest investors in private credit funds. Recently, private credit firms have been exploring ways to provide retail investors with access to funds that were once only available to accredited investors.

With the recent additions of Blackstone and KKR into the S&P 500, and the potential for more alternative investment managers to be added soon, this could add a whole new sub-sector to the Financials sector. This paper delves into the genesis of private credit, the role of private credit, its pros and cons, and whether private credit and traditional banking can coexist.

Private credit defined

Private credit is lending made by non-bank entities, such as private credit funds, that work directly with borrowers. These funds hold the debt, unlike traditional banking where the debt can be resold to other investors. Traditional lending uses syndicated lending, which is a group of lenders, typically a consortium of banks and financial institutions, that work together to provide a loan to a single borrower.1

Private credit is an alternative source of financing for businesses, particularly those that may not have access to traditional bank loans or public debt markets. Historically this has been businesses with annual revenues between $10 million and $1 billion, but this has changed over recent years as larger companies have started utilizing private credit funding.2 Private credit does not include bank loans, broadly syndicated loans, and funding provided through publicly traded assets such as corporate bonds.

Non-bank lenders like insurance companies, private debt companies, and business development companies, lend directly to the small and middle-market companies that do not have or have had trouble getting traditional bank financing. Private debt loans offer unique terms and conditions to meet specific needs of the borrower as well as the lender. Collaborating directly with the borrowers gives private credit lenders more control over documentation, which provides more favorable terms and flexibility for the borrower. Additionally, working directly with the borrower produces faster results and better execution certainty when compared to syndicated loans.3

Origin of private credit

Private credit originated in the 1980s when insurance companies acted as direct lenders to companies with strong credit histories. However, the industry saw substantial growth after the 2008 financial crisis, when increased regulatory restrictions on banks led to traditional lenders cutting back financing, giving rise to private credit as a viable financing option. Since the Great Financial Crisis, private credit has become a direct competitor with traditional bank lending.

According to Preqin, closed-end private debt funds have increased their assets under management from

around $500 billion in 2015 to around $1.7 trillion as of the end of 2023.4 Private credit managers do not

face the same level of regulatory scrutiny as traditional banks. According to Bloomberg, The Securities and

Exchange Commission introduced rules that called for

external audits on private fund advisors’ asset values,

but these rules have been overturned in appeals

court.5 In addition to the less onerous oversight from

regulators, private credit funds can be more flexible

and accommodating with loan terms than traditional

banks. Syndicated loans, which involve many lenders,

often have terms that are fluid up until the loan

closing, whereas private credit lenders work directly

with the borrower to determine appropriate terms,

conditions, and prices. These are typically held by the

credit manager rather than re-sold to other investors

like with syndicated loans.

According to Preqin, closed-end private debt funds have increased their assets under management from

around $500 billion in 2015 to around $1.7 trillion as of the end of 2023.4 Private credit managers do not

face the same level of regulatory scrutiny as traditional banks. According to Bloomberg, The Securities and

Exchange Commission introduced rules that called for

external audits on private fund advisors’ asset values,

but these rules have been overturned in appeals

court.5 In addition to the less onerous oversight from

regulators, private credit funds can be more flexible

and accommodating with loan terms than traditional

banks. Syndicated loans, which involve many lenders,

often have terms that are fluid up until the loan

closing, whereas private credit lenders work directly

with the borrower to determine appropriate terms,

conditions, and prices. These are typically held by the

credit manager rather than re-sold to other investors

like with syndicated loans.

The prolonged low-interest rate environment, starting in 2011 when the 10-year yield was below 2% until 2020 when the 10-year yield had a sub 0.60%, allowed private credit to flourish. Investors were attracted to the higher yields and hopes of enhanced returns.6 The combination of the Great Financial Crisis, low-rate environment, and the tightening of lending standards by traditional banks has been responsible for the material growth seen in private credit over the last 15 years.

Types of private credit

There is an assortment of private credit strategies. Below are the most common strategies and some of the biggest players in each area:

- Direct Lending: As of the end of 2023, within the private credit space, direct lending was the largest private credit strategy with 46% of assets under management.8 Direct lending generally involves senior loans made to middle markets without the use of an intermediary but may include credit lines and second lien loans. The largest manager of direct lending funds is Ares, with approximately $120 billion of AUM.9 Blackstone, Blue Owl, and KKR are also major players in direct lending space.

- CLOs: A collateralized loan obligation is a security backed by a pool of loans, which can include hundreds of individual debt issuances that are classified into different tranches relative to risk levels and yields. What was once considered a niche/esoteric investment vehicle has now become commonplace in many corporate bond portfolios. U.S. investors typically receive a floating rate return based spread off SOFR (secured overnight financing rate). The largest CLO managers at the end of 2023 by AUM are Carlye (~$38bn), Golub Capital (~$38bn), and Blackstone (~$37bn).10

- Distressed Credit: This is a private credit strategy where the fund purchases corporate debt that is trading at a substantial discount to its original value. Lenders in distressed debt try to find good companies with bad balance sheets and try to identify fulcrum securities, which are the most subordinated part of the capital stack to be paid back in a bankruptcy or restructuring.11 Notable distressed credit players are Ares, Brookfield, and Blackstone.

- Credit Special Situations: Sometimes called “event-driven credit”, this strategy focuses on corporate events, such as restructurings, spin-offs, M&A, litigation, activism, corporate restructurings, etc. The underlying investments are driven by company specific events rather than market movements.12 Notable players in this segment are Ares and Apollo.

- Mezzanine Lending: Is a hybrid investment using both debt and equity. By combining higher risk debt that sits in the middle of the capital stack, so a later claim on assets in the event of a bankruptcy and using equity as a form of collateral. This type of financing is used sometimes when firms have a senior debt provider such as a bank, but still in need of additional funding to cover the entire gamut for a specific deal. Leverage buyout deals often include mezzanine financing because it allows firms to increase their leverage ratio, thereby reducing the amount of equity required. Mezzanine financing often allows for more flexibility in LBO structures compared to senior debt, with features like Payment-in-Kind (PIK allows for borrowers to pay interest with additional debt or equity, rather than cash). Blackstone, KKR, and Apollo have prominent funds in this space.

- Sector-Specific Debt: This includes infrastructure, real estate, and venture debt are all examples of this type of private credit. Infrastructure loans typically have a longer tenure, in some cases 30 years plus that support development of infrastructure assets. On the other hand, venture debt involves startups that have yet to turn a profit. Like mezzanine lending, PIK financing can be used to alleviate the burden of near-term debt servicing costs within venture debt. Brookfield and Ares each have prominent infrastructure funds in this space.

Current and future landscape

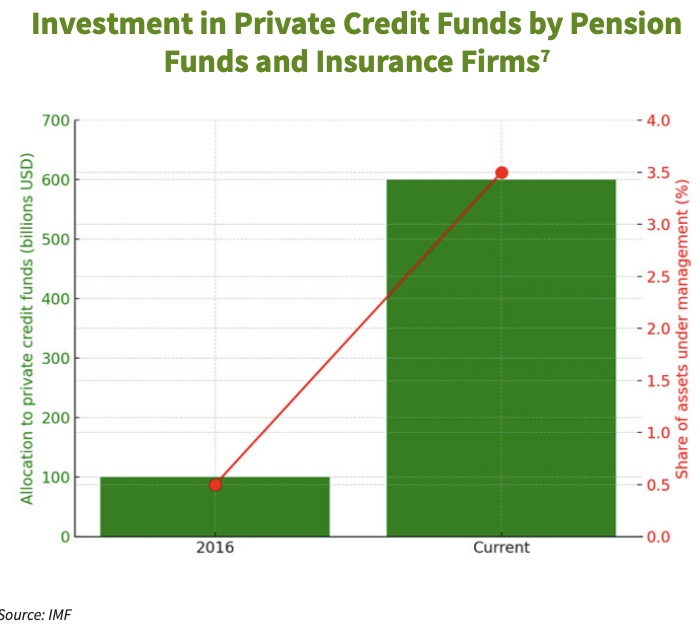

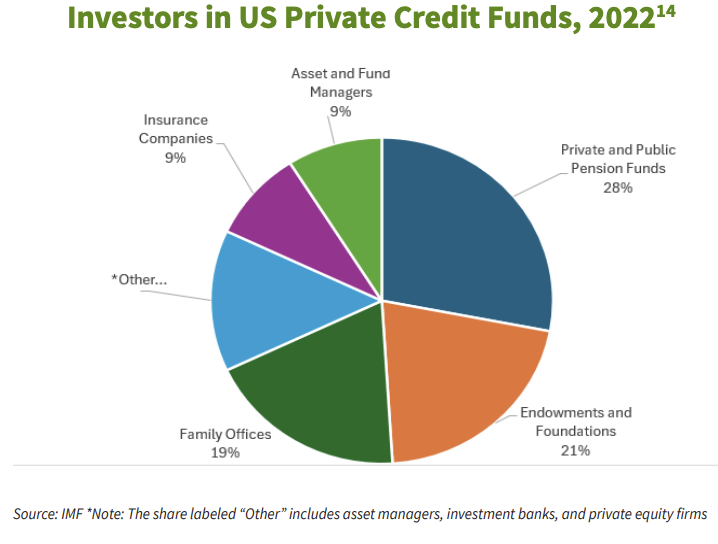

Private credit today is mostly used by institutional investors like pension funds, insurance companies, sovereign wealth funds, family offices, and foundations & endowments. These investors are drawn to private credit because of its diversification, low correlation with other assets, and yield enhancement characteristics. Recently, alternative managers of private credit funds have been looking to enter the personal wealth market by offering retail investors through interval funds (closed-end investment that offers to repurchase a portion of its shares from investors at regular intervals). Interval funds often have minimum investments as low as $1,000 that can be purchased in brokerage accounts, whereas larger investments that typically require more complex subscriptions agreements.13

Alternative asset managers in private credit have

achieved success through acquisitions and joint

ventures. Two noteworthy acquisitions in recent

years were Apollo’s acquisition of Athene and KKR’s

acquisition of Global Atlantic. Alternative investment

managers are attracted to life insurance companies

to gain access to substantial capital and a large

portfolio of assets under management, which can

then be invested as the firm seems fit. A recent study

by Fidelity showed that about 73% of insurance assets

are invested in traditional fixed income investments,

estimated to be around $25 trillion.15 A Blackrock

survey revealed that roughly 90% of insurers expect

to increase their allocations to alternatives over

the next few years, with an expected weighted

average increase of 3%. Given the $25 trillion in

fixed income assets held at insurance companies,

a 3% reallocation would imply a flow of $750 billion into alternatives. With AUM of $1.7 trillion in private

credit as of the end of 2023, Blackrock is projecting private credit will surpass $3.5 trillion by 2028.16

Alternative asset managers in private credit have

achieved success through acquisitions and joint

ventures. Two noteworthy acquisitions in recent

years were Apollo’s acquisition of Athene and KKR’s

acquisition of Global Atlantic. Alternative investment

managers are attracted to life insurance companies

to gain access to substantial capital and a large

portfolio of assets under management, which can

then be invested as the firm seems fit. A recent study

by Fidelity showed that about 73% of insurance assets

are invested in traditional fixed income investments,

estimated to be around $25 trillion.15 A Blackrock

survey revealed that roughly 90% of insurers expect

to increase their allocations to alternatives over

the next few years, with an expected weighted

average increase of 3%. Given the $25 trillion in

fixed income assets held at insurance companies,

a 3% reallocation would imply a flow of $750 billion into alternatives. With AUM of $1.7 trillion in private

credit as of the end of 2023, Blackrock is projecting private credit will surpass $3.5 trillion by 2028.16

Private credit pros & cons

The benefits of using private credit from a borrower’s standpoint, specifically direct lending, are:

- Direct lenders can close loans faster because there is considerably less red tape compared to syndicated loans.

- There is no need for ratings, which allows for faster execution and more tailored loan terms without being constrained by the standardized requirements that come with rating agencies.

- There is greater certainty of pricing and dollar amount of the loan.

- Confidentiality is preserved.

The benefits for investors in private credit are:

- Higher yields you can receive versus traditional bonds and loans to compensate for the illiquidity of the private credit market.

- Outperformance in recent years - private credit has outperformed both the S&P 500 and MSCI All World Index going back to 2000.17

On the flipside, private credit carries many obvious risks for both the borrower and investor in a private credit fund:

- Illiquidity is the first risk that potential investors point to, largely due to the limited secondary trading in private credit. Recently at a JP Morgan conference, Kipp deVeer, Head of Ares Credit Group, mentioned that secondary liquidity could be a long way off because direct lenders originate to hold.18

- Due to the illiquidity of private credit funds, their structure is designed to limit liquidity and maturity transformation risk through long-term lockups, so investors are unable to free-up their funds.

- Unrated – private credit loans are lightly regulated and much more opaque than public markets. Because of this lack of transparency, it could be difficult to detect rising risks in advance.

- Floating rates are common with private credit. Borrowers may face rising financing costs and perform poorly during downturns, potentially causing significant losses for investors in private credit funds.

- Retail investors often lack a thorough understanding of the specialized risks associated with private credit.

How do both coexist

Private credit has seen a significant increase in assets under management since the Great Financial Crisis, yet traditional banks continue to play an integral role for private credit firms. Traditional banks are leading suppliers of leverage to these private credit firms. In 2021, private credit firms borrowed nearly $200 billion from US banks, however, this figure represents less than 1 percent of banks’ assets according to the Federal Reserve.19

One example of how banks and private credit companies have been working together recently is through synthetic risk transfers (SRTs). These instruments function similarly to a credit default swap, allowing banks to transfer some of their riskiest loans (commercial loans, mortgage loans, and auto loans) to alternative managers. Meanwhile, the underlying assets remain on the bank’s balance sheet. Private credit companies are compensated by the banks in the form of monthly interest payments, which typically carry a high fixed payment. The private credit company assumes responsibility for the losses that occur on the existing pool of assets that the bank has bought protection. While European banks have used SRTs for years, U.S. banks are increasingly adopting this instrument. The growth of SRTs by U.S. banks is driven by their willingness to free up capital without having to sell assets at a loss or raising dilutive financing, and most of all it is an efficient way to comply with Basel III and Basel IV guidelines. As the banking industry moves further away from the SVB and other bank failures of Spring of 2023, what was once perceived as a major shift for U.S. banks has since been moderated in commentary from the Fed. If banking regulations become less stringent, it is reasonable to assume that banks may use SRTs less frequently.

Private credit and public lending can coexist and complement each other under various market conditions. Public lending is attractive for borrowers when lending standards are loose, primarily because public credit carries much lower interest rate than private credit. In such an environment, private credit may struggle to compete, and traditional lenders outperform. Conversely, private credit becomes more relevant when lending conditions tighten, as seen in recent years. For borrowers seeking more flexible loan structures (e.g. payment-in-kind) or those with sub-investment grade credits and second liens, private credit is often the preferred option. In this backdrop, you could see more lending opportunities for private credit companies and the potential for stock outperformance.

When bank regulators first announced the Basel III Endgame/ Basel IV proposals, Jamie Dimon, CEO of JP Morgan, joked at a Bernstein industry conference in June that private equity lenders were likely “dancing in the streets” due to the potential windfall of business coming from traditional banking to private credit managers.20 At the same Bernstein conference, executives from Blackstone and Apollo were making the case that private credit funds do not have the bank run risk that plagued Silicon Valley and First Republic banks in the Spring of 2023, and went further in discussing the asset-liability mismatch that led to the collapse of both banks. With the recent additions of Blackstone (added 9/18/2023) and KKR (6/24/2024) to the S&P 500, and with other alternative managers like Apollo with a market capitalization of over $63 billion and Ares with a market capitalization of over $44 billion, both companies could be candidates to be added to one of the most widely followed indices in the world. The additions of these alternative asset managers to the S&P 500 provide large-cap financial services analysts more tools to use in different market environments. No matter what side you stand on, most investors would agree that both traditional banking and private credit can coexist, but both investors and borrowers need to have a strong understanding of the products and challenges of each market to determine which approach is most suitable.

References:

- https://markets.jpmorgan.com/research/email/scx/-bmk6jog/t0BcwOlKhpePpHiXHdmH4Q/GPS-4733967-0

- https://www.federalreserve.gov/econres/notes/feds-notes/private-credit-characteristics-and-risks-20240223.html#:~:text=What%20is%20Private%20 Credit%3F,)%2C%20to%20fund%20private%20businesses

- https://www.federalreserve.gov/econres/notes/feds-notes/private-credit-characteristics-and-risks-20240223.html#:~:text=What%20is%20Private%20 Credit%3F,)%2C%20to%20fund%20private%20businesses

- https://www.bloomberg.com/news/articles/2024-02-20/what-is-private-credit-how-does-it-work-and-what-are-the-risks

- https://www.bloomberg.com/news/articles/2024-02-20/what-is-private-credit-how-does-it-work-and-what-are-the-risks

- https://fred.stlouisfed.org/series/dgs10

- IMF Data

- https://markets.jpmorgan.com/research/email/scx/-bmk6jog/t0BcwOlKhpePpHiXHdmH4Q/GPS-4733967-0

- Factset Data

- https://markets.jpmorgan.com/research/email/scx/-bmk6jog/t0BcwOlKhpePpHiXHdmH4Q/GPS-4733967-0

- https://research.wolferesearch.com/file/35577.pdf?docRef=141a5d7e-4128-44ad-a5f6-362d0a3b3e11&uid=fe463e68-e8c1-4a53-9348- 43f9c1893c82&jobRef=ab0bdd51-ffa6-4856-ac9c-bfaa42d4f5c5

- https://www.destracapital.com/about/insights/what-special-situations-credit-investing

- https://www.bloomberg.com/news/articles/2024-08-01/private-credit-sells-funds-for-small-investors-as-big-ones-balk

- https://www.imf.org/en/Home

- Fidelity

- https://www.brookings.edu/articles/what-is-private-credit-does-it-pose-financial-stability-risks/

- Factset Data

- https://markets.jpmorgan.com/research/email/scx/-7slci8e/a2fcc6a2-11aa-428b-a3e3-5921bfe2488c/GPS-4773633-0

- https://www.federalreserve.gov/publications/files/financial-stability-report-20231020.pdf

- https://finance.yahoo.com/news/wall-street-is-divided-over-the-rise-of-private-credit-140058228.html

Related Insights

-

Article

10 min read

Article

10 min read

-

Article

-

Article